Understanding the insurance claims process

We are fully aware that the majority of drivers have a rough idea of the processes involved if they were to experience an accident – the steps they would need to take to inform their insurance provider, and the details they would need. But would they know what happens next?

Unless you have experienced the insurance process first-hand, you are unlikely to understand the inner-workings of determining how to decide whether your vehicle can be deemed road-worthy or not.

We have provided this guide to give you behind the scenes access to how insurance providers check your beloved vehicle to see whether you can enjoy its company for a little longer, or have to say an emotional goodbye.

What happens after an accident?

Driving brings some inherent risks with it – and the potential for crashes and accidents to occur.

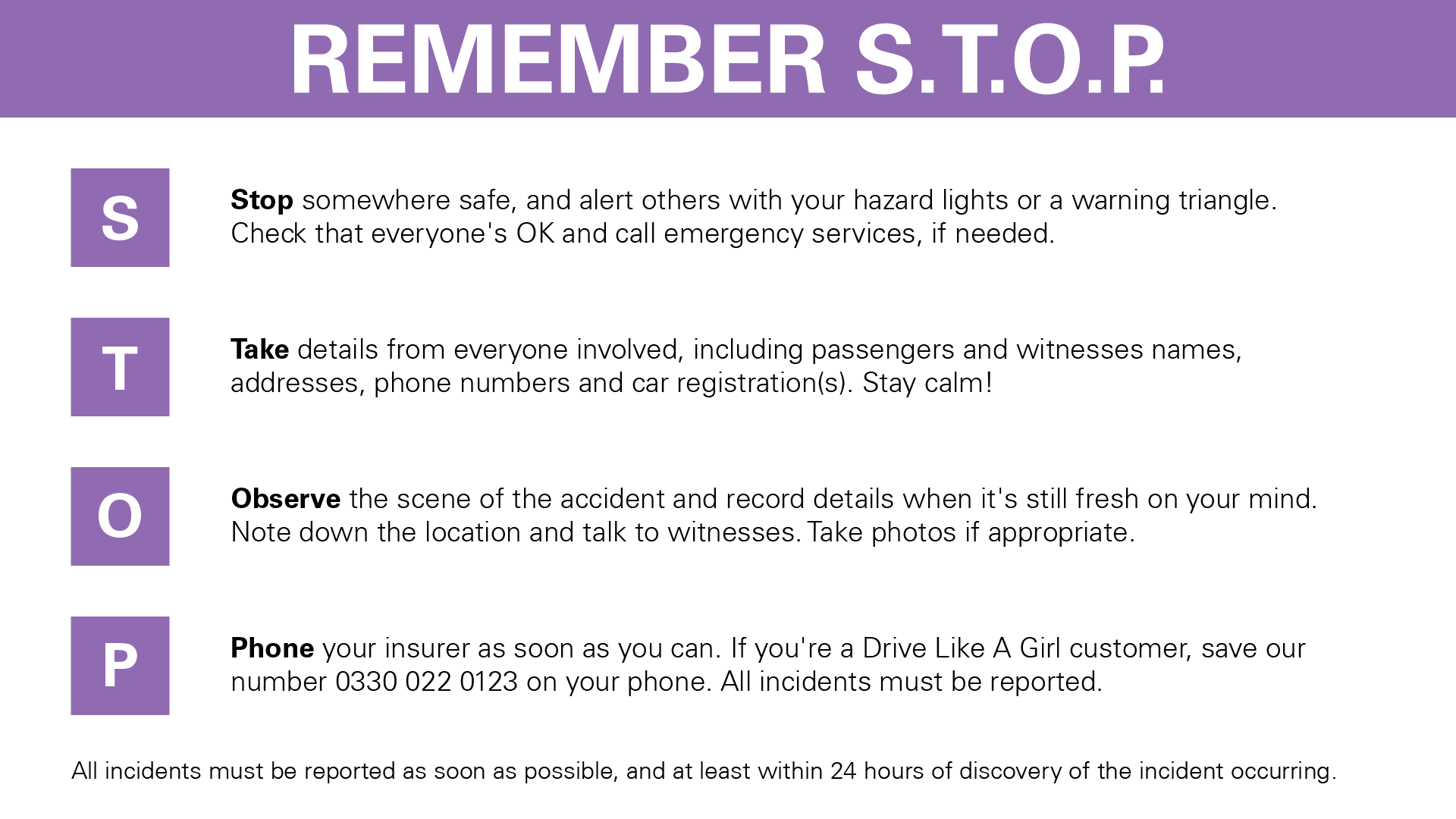

There are a few simple steps every driver should memorise, if they ever find themselves in this situation. We advise our customers to remember ‘STOP’:

Follow these steps to make sure you gather all the information you need for your insurance company – these will be essential in the overall claims process.

If you are a drive like a girl customer, speak to us on 0330 022 0123 before you make any arrangements for replacement or repair.

Informing us first will help with your claim process and reduces the chance of being a victim of fraud.

Once you’ve contacted us, we can take care of all the necessary arrangements e.g. to repair the damage to your car and provide you with a temporary replacement car.

But, what happens if your insurance provider tells you that your car is written-off?

What is an insurance write-off?

Firstly, we do not want to overly-complicate this issue, so simply put, a write-off falls into two primary categories:

- It would be unsafe to put your car back on the road, or

- It could be safe to drive again, but would cost too much to repair.

This is worked out using a series of complicated algorithms which checks the repair-to-value ratio, amongst other aspects to determine whether it is cost-effective to perform repairs or to provide you with the value of the vehicle (at the time of the damage).

It is important to note that not every claim means that a car will be written off – a small amount of damage to your paintwork won’t cause an insurer to ban your vehicle from the road. However, if it does not work out to be cost-effective, then your car may be ‘written-off’ by your insurer.

If you receive a ‘write-off’ declaration, you will also receive a categorisation for the amount of damage and whether it is deemed roadworthy – this will let you know whether your car will ever see the road again!

What are the vehicle write-off categories?

When your car is involved in an accident, it will need to be inspected by an ‘appropriately qualified person’ and issued with a categorisation relating to the amount of damage received, according to the Association of British Insurers (ABI).

Your car will fall into one of four categories: A, B, S, and N:

- Category A: Scrap

This vehicle is deemed not suitable to be repaired. Must be crushed without any parts being removed. This vehicle will be classed as waste.

- Category B: Break

The vehicle is deemed not suitable to be repaired, and declared a ‘Break’. Usable parts can be recycled. This vehicle will be classed as waste, and the chassis of the vehicle can never be used again and must be crushed.

- Category S: Repairable (Structural Damage)

Repairable vehicle which has sustained damage to any part of the structural frame or chassis and the insurer has decided not to repair the vehicle.

- Category N: Repairable (Non-Structural)

Repairable vehicle which has not sustained damage to the structural frame or chassis and the insurer has decided not to repair the vehicle.

So, if you are wanting to hang onto your beloved vehicle and receive a Category S or N distinction, you may perform the necessary repairs and get back on the road. But do note that this may be an expensive endeavor – your insurance provider would have seen it as economically unviable, and CHOSEN not to put it back on the road.

Also, please note that your insurance may increase if you drive a vehicle carrying the Category S or N sticker, once it has been repaired.

It is never safe to try and repair a category A or B vehicle and they should never be driven on the road again.

Can I repair a written-off car?

If you have chosen to repair your vehicle, you will have to buy the car back from your insurer – don’t worry this is not an additional charge; when your insurance company has given you a pay-out/ settlement figure, you can (usually) buy the vehicle back using these funds.

Note: Tell your insurance about your ambition to buy your car back as soon as possible, before scrapping has begun.

But who exactly can perform these repairs?

Once a claim is made and your vehicle is given a classification, you will need a professional to repair your car and deem it to be safe to drive once again.

You should leave all repair work to a professional automotive mechanic, who is a registered member of The Institute of Automotive Engineer Assessors.

Will my insurance go up if I insure a previously written-off car?

So you’ve made all the essential repairs to your car, and it’s now ready, once again to hit the road. You may realise this price has gone up significantly more than its original state. This is because these vehicles are a higher risk to insurers – some might not cover you.

Unfortunately, this is a side-effect of choosing to restore your Category S or N vehicle and should be carefully considered prior to purchasing your written-off vehicle from your insurer.

It may not be economically beneficial to undertake this process. So watch out!

What forms do I need to make my car road-worthy again?

When you have registered this interest, and received your car back, you will be able to make repairs on the car.

You will also most likely be asked to provide a copy of the repair invoice and post-repair MOT certificate before your insurer confirms you are covered.

Also according to the DVLA, you also need to:

- Send the complete logbook to your insurance company

- Apply for a free duplicate logbook using form V62

If you do not inform the DVLA of the new-found status of your vehicle, you could be charged £1000.

Will I need to declare the previously ‘written off’ status of my car if I choose to sell in the future?

Yes, is the simple answer.

It is a legal requirement to declare whether your car has been written-off in the past. This is a requirement so that buyers’ are protected against any unexpected problems with the car.